Most fully-insured employers are flying blind into their annual health plan renewals. Without claims data, finance and HR professionals have no way of knowing what to expect. So, if you’ve ever gotten a steep renewal rate, or you’re facing one now, read on. First, we’ll explain how your insurance carrier determines your health plan premiums. Then, we’ll look at two common scenarios that can inflate your operational expenses by as much as six-figures:

- You’re facing a double-digit renewal, or

- You got a single-digit, trend, renewal this year—but it’s built on the back of a previous bad renewal.

We’ll also provide guidance on what you can do to correct course and reduce costs.

The Carrier’s Most Important Metric

For background, an insurance carrier uses a medical loss ratio (MLR) to drive their business forecast and determine the health plan premium rates they charge. MLR is typically benchmarked at 85%. This means the carrier expects to pay out 85% of the premiums they collect for healthcare expenses.

- Above an 85% MLR: your group has an “unhealthy” risk profile

- Below an 85% MLR: your group has a “healthy” risk profile

The Dreaded Double-Digit Renewal

If you’re above an 85% MLR, you’re about to get a bad renewal. And your carrier will likely deliver this news as late as possible. It’s a strategic play on their part. Doing so compresses the timeline for you to do anything about it. They’re betting you’ll just suck it up.

Your hand is ruined for a competitive bid.

Even if you wanted to do something, your hand has been shown. Other carriers don’t have your claims data, and they can only infer your group’s health based on the bad renewal.

However, understand that your health risk profile is fluid.

Due to employee turnover, your company’s health profile can change dramatically throughout the plan year. Maybe one or two employees with chronic conditions left, and you hired 20-30 younger or healthier employees. Or, maybe your health risk was artificially inflated due to a statistical anomaly (like an unusually high number of babies being born). It's entirely possible a bad renewal rate doesn't accurately reflect your group's current health profile. It may have improved.

Inspecting a Trend Renewal

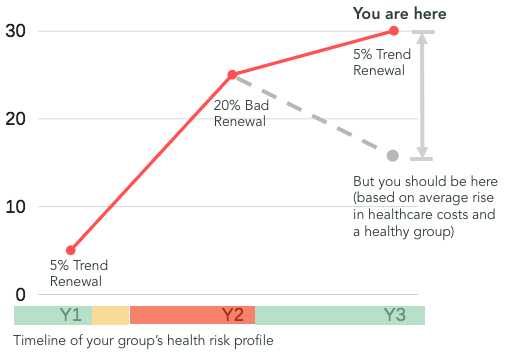

A trend renewal is typically considered a 5-8% increase in your healthcare premiums. This range is generally accepted as the annual increase in health care costs for the U.S. You might be so relieved to get a trend renewal that you lose sight of the bigger picture. One “good” trend renewal after a bad renewal is still substantially inflating your costs. Likely six-figures. And possibly high six-figures.

A single bad renewal will continue to inflate your costs year after year, even when your group profile becomes healthy.

In the carrier’s model, renewals always go up.

When your health profile goes from unhealthy to good, the carrier doesn’t correct course so your renewal is back to where you should be for a healthy group. Instead, they issue a trend renewal.

But… what if my bad renewal really is fair?

If your group currently has an unhealthy risk profile, there are still steps you can take to mitigate a double hit: you’re paying more in premiums, and your employees are paying more in premiums. Look at your plan choices. Optimize your plan design to incentivize your healthy employees to elect a High Deductible Health Plan (HDHP) paired with a Health Savings Account (HSA). This can be a strategic way to reduce premium costs for both you and your employees without sacrificing benefits.

Tap Us In, and Find Out

Lumity brings to the midmarket the kind of data insights that are typically only available to self-funded, big companies, so your renewals move in sync with your actual health risk profile. Our proprietary risk modeling will reveal whether your renewal rate is fair, and we’ll review your plan structure. For a complimentary benefits assessment, we invite you to contact us today.