We at Lumity tend to hail the existence and use of Health Savings Accounts (HSAs) more often than not, partially because our customers tend to have younger, relatively healthy individuals and families in their group that benefit from the selection of High Deductible Health Plans (HDHPs) - but also because HSAs provide individuals with a means to self-insure while the risks are ostensibly low.

Of course, a personal decision to choose HSA-qualified HDHPs is more involved than the above characteristics, so in this Lumity Spotlight Series we will cover the benefits, uses, and common considerations regarding HSAs and HDHPs, starting with a basic overview.

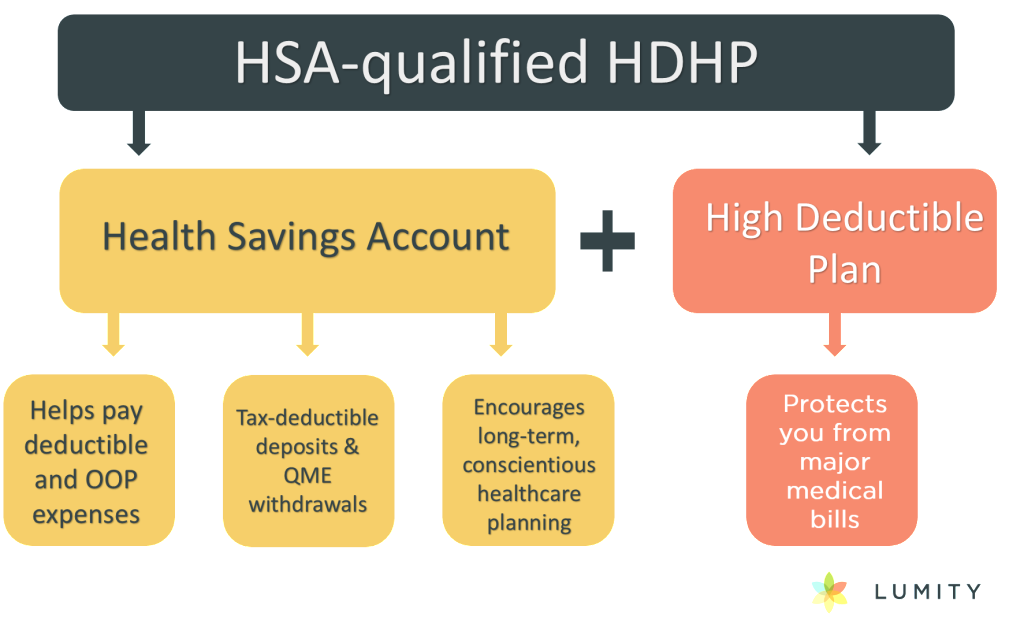

An HSA is an employee owned, pre-tax, rollover savings account intended to be used specifically for Qualified Medical Expenses.

So, HSAs are unique savings accounts but not in any way most of us can’t understand. Similar to how banks have restrictions and rules on how you qualify and can use certain accounts – HSAs have restrictions as well – but these restrictions come from the government.

First and foremost, you must be covered under a specifically defined HDHP to be eligible for an HSA. “High deductible” is defined by specific minimum deductible and maximum out-of-pocket (OOP) costs.

Beginning in 2016, individuals with Single coverage need aminimum deductible of $1,300 with a max OOP of $6,550. This means at a minimum you need to be on the hook for at least $1,300 dollars of your healthcare costs before your insurance kicks in and the most you can be charged afterwards is $6,550. This is good to know because the most you can contribute to your HSA as an individual is $3,350.

Those with Family coverage need a minimum deductible of $2,600 with a maximum OOP of $13,100 and the most they can contribute to their HSAs is $6,650.

Another excellent incentive for those who are fifty-five years or older, is that the government allows a Catch Up Contribution of $1,000 on top of the Individual and Family limits.

We like HSAs, generally, for the following reasons:

They save and re-purpose money

HDHPs mean higher deductibles, yes – but if you and/or your family hardly go to the doctor outside of regular checkups and the holiday flu, you’re probably not paying more than the savings you get in lower premiums. But alas! Even if you are, using money from your HSA could still essentially save you money because of the next reason we love them so much…

They are tax preferred

The federal government, and most state governments with the exception of Alabama, California, and New Jersey, won’t count money you put in your HSA as part of your income during tax day, similar to money you put in a 401(k). So even if you max out your HSA and your OOP on an HDHP, you’re still saving approximately 20% of the $3,350 or $6,650 you spent to get better. If you know how much you’re saving and know how much you’ll likely spend, you can make a more informed decision on whether this is a good deal or not. Which leads us to our next reason for liking HSAs.

They encourage conscientious health care planning

Planning is an amazing stress reliever that more people should take advantage of. Face it, many of us need a reason to stay diligent and disciplined and we think of health insurance like we think of tax day – a headache only once a year. But unlike taxes, which we dread to mess up because of the financial consequences, we don’t act like we fear the physical and financial consequences of poorly or unplanned health care decisions. HSAs fundamentally encourage us to plan better for our health care needs because we have to consider how much we’re likely to spend on healthcare for an entire year we make the decision to gamble on HDHPs.

Coming up next, and forgive us for taking it to the lecture hall, we’ll be talking about HSAs and the Inherent Gamble of Health Insurance -- subscribe to keep up to date on the latest Lumity Spotlight Series.

You can alleviate some of the worry when considering health plans using estimates of OOP expenses and value-driven health plan recommendations with Lumity’s data analytics technology. Give us a call at 1-844-2-LUMITY and find out more about how data makes a difference.