When it comes to compliance with the employer mandate of the Affordable Care Act (ACA), you are responsible for ensuring that you not only provide coverage to your full-time employees if you're an applicable large employer, but also that your plans are affordable and provide minimum value.

Because the law went into full effect in 2016, the vast majority of insurance carriers only offer compliant plans to take care of the minimum standards of plan designs. But - Lumity wants to make sure you know what that means.

Affordability...for your employees, not your company

The IRS considers your employee health plans affordable as long as employees aren't required to spend more than 9.5% of their household income on their share of the cost. Since it would be unreasonable to expect employers to know and find out an employee's true household income without invading their privacy, there are three safe harbor methods you can use to determine this:

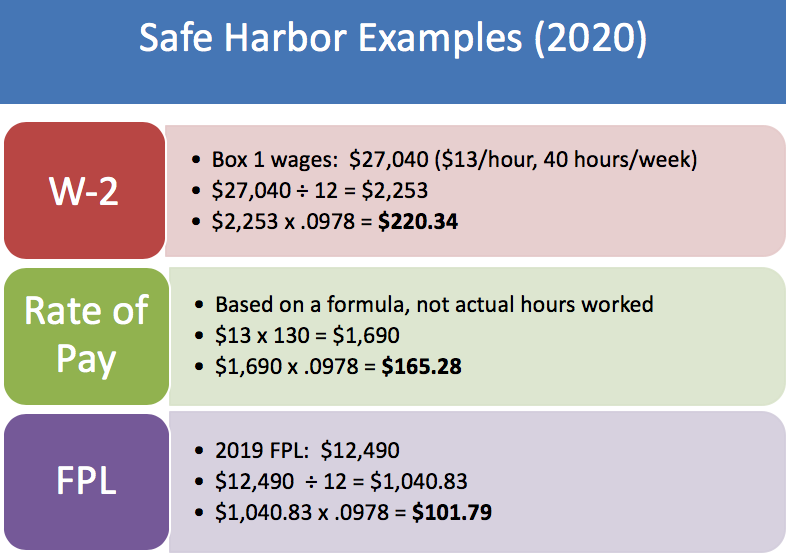

- Determine 9.5% against your employee's annual W-2 wages.

To use this method, your employee's required contribution must remain a consistent amount or percentage of their W-2 wages for the entire calendar year. You're not allowed to make discretionary adjustments to this and the wages should also be reduced for any salary deductions under a 401k or cafeteria plan. This could present some problems for you if you have hourly or variable-hour employees that aren't salaried since you won't know what their annual wage is until the end of the plan year. - Determine 9.5% against an employee's rate of pay.

This is likely beneficial if you have hourly workers. You'll want to take an employee's hourly rate and multiply it by 130 hours per month. This, rather than their actual monthly wage, is the determining factor for affordability. Make sure you're not charging them more than 9.5% of that amount each month for their share of health plans. - Determine 9.5% of the Federal Poverty Level (FPL) for a single individual.

While this is the easiest method you could use, it's also probably the most expensive for you. Using the federal poverty level method, you can basically have a predetermined maximum employee contribution that will always result in your plans being affordable to employees. The FPL for 2020 is $12,490, which translates to a maximum employee cost of $1,040.83 for their health plans.

Minimum Value

This is where you hear terms like Gold, Silver, and Bronze plan. This has to do with the claims payments of the plans you choose - not how much you pay for them. As long as your plans pay at least 60% (bronze plan) of the cost of medical services to those covered, your plan provides minimum value. Be sure to have your broker, legal or financial counsel go over the plans and ensure they are compliant.

Lumity can help with these questions about ACA compliance and more. Subscribe to our blog or follow us on Linkedin and Twitter to get our latest information as it happens.

Cheers to better benefits!