Where we last left off in this series, the key takeaway was “money talks”: finding your employer contribution sweet spot incentivizes further employee Health Savings Account (HSA) uptake. But after the right employer contribution is in place, there’s a third step you can take to boost adoption. Let's look at what you can do to mitigate employee risk with your plan design.

- Step 1: Seed Early Adopters

- Step 2: Find Your Employer Contribution Sweet Spot

- Step 3: Mitigate Employee Risk with Your Plan Design

- Step 4: Educate Employees

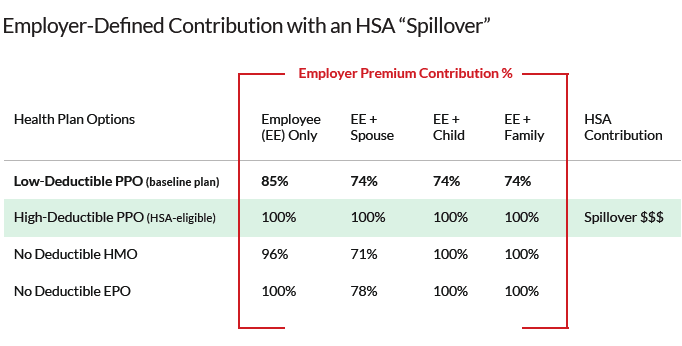

Pay 100% of the High-Deductible Health Plan (HDHP)

Going all-in and paying 100% of the HDHP premium can significantly reduce the perceived financial risk of a high-deductible health plan. Optimize your plan design so employees can clearly identify the value-difference between health plan choices:

- Lower deductible plans will have an employee cost-sharing portion

- The high-deductible plan won’t (due to the lower cost of the premium)

Benchmark your employer premium contribution to a set amount that enables the HDHP plan to be free with an HSA “spillover.” Doing so is the optimal way to set up your benefits package.

In the example:

- The employer contribution is baselined to the richer, low-deductible PPO;

- 85% of the employee-only low-deductible premium is paid by the employer;

- This amount more than covers the lower premium of the high-deductible plan;

- Now the high-deductible plan is essentially “free” for the employee;

- There’s a potential for any overage to “spillover” to the HSA.

Next up, Employee Education

HSA survey respondents who cited a “lack of employee understanding” (51%) had lower HSA adoption rates. So, we'll wrap up the series with two tactics you can apply to encourage HSA uptake.

As always, if you’d like help boosting your HSA participation, we're happy to provide a free consultation. Lumity has experience driving significant HSA participation for companies like Greenhouse, GoFundMe, and SquareTrade.