For most U.S. employers, providing employee health care coverage is a cost of doing business, not your core business. And it's the second largest operational expense after wages. Yet HR and finance professionals have little—or no—visibility into this expense.

How bad is it?

If you're wondering what you're up against, it's well worth your time and money to read this ProPublica exposé: Insurers Hand Out Cash and Gifts to Sway Brokers Who Sell Employer Health Plans:

Human resources directors often rely on independent health insurance brokers to guide them through the thicket of costly and confusing benefit options offered by insurance companies. But what many don't fully realize is how the health insurance industry steers the process through lucrative financial incentives and commissions. Those enticements, critics say, don't reward brokers for finding their clients the most cost-effective options.

So, the question is, how can you possibly know if you're getting a fair health plan renewal?

Renewal Assumptions

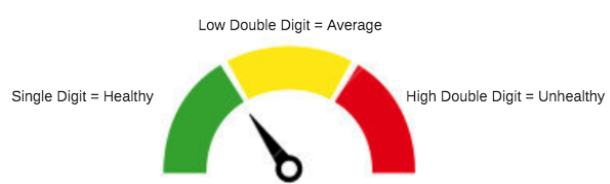

Employers typically assume their renewal rate is an accurate reflection of their claims performance.

We’re conditioned to think that a single-digit renewal means your group is healthy. But the critical question is “how healthy?” (Or “how average”? Or “how unhealthy”?)

The Reality

Your annual renewal is like playing poker against the house. For fully-insured companies, the standard process favors health insurance carriers because they hold all the cards.

Your carrier has the advantage of knowing your employee medical claims and prescriptions, and they’re betting that you don’t have this information.

Carriers Manage Risk Like a Casino

Your insurance premiums are being managed like a casino’s portfolio, and the house doesn’t lose.

The risk is being shifted to you.

Insurance carriers will tout the indisputable rising cost of health care and how their own risk is going up. And there’s something to this, especially with the loss of government subsidies and other legislative risks. But what they don’t publicize is how they’re distributing the risk. Carriers manage their portfolios in any risk environment. And, a lot of padding goes into your renewal and premiums. In an ideal world, if your group’s healthcare cost came in below the carrier’s forecast, you’d get a negative renewal.

Your renewal hikes aren’t necessarily tied to your own company’s health risk.

You’re essentially paying a “risk tax” on the broader portfolio of business the carrier is managing. They load balance and move more risk premium onto your rates to offset losses elsewhere on their books.

Broker commissions are tied to premiums.

Also, understand how most benefits brokers are compensated. The more you pay in premiums, the more your broker gets paid. Their commission structure is inversely tied to you getting a good renewal.

How to Get a Fair Renewal Rate

lifts the lid on how health plan renewals are usually run from an insurance carrier and brokerage perspective. It also describes measures you can take to ensure your plan rates are in line with your group’s actual health risk profile. Because most employers are way overspending for what their employees actually get.

Download your copy today.